What happens when you strip away the hype and put some of the market’s most beloved stocks under a cold, analytical microscope? In this episode of In the Money with Amber Kanwar, Amber is joined by Sam LaBell, Portfolio Manager at Veritas Asset Management, for a brutally honest reality check on what investors own — and why some of those positions may be riskier than they look.

Pro Picks is brought to you by ATB Financial. With $62 billion in assets, ATB Financial is powering possibilities for more than 820,000 financial services clients in Alberta and beyond. ATB’s Capital Markets arm is a full-service investment dealer that offers investment and corporate banking, sales and trading, institutional research, and risk management. Visit www.ATB.com/inthemoney for more information.

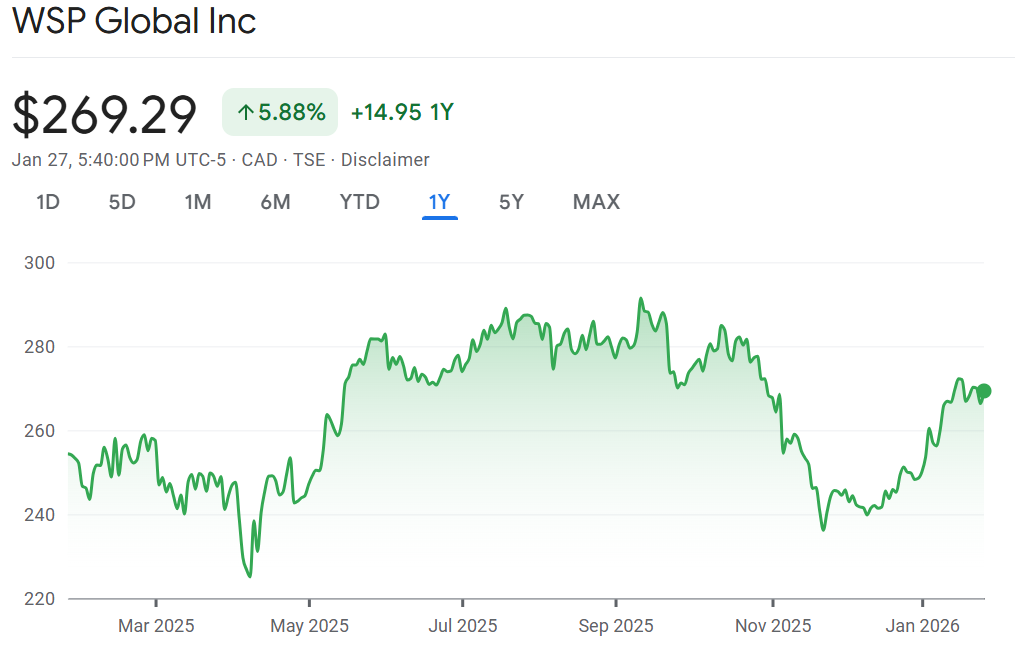

- Acquisition-Driven Platform for Scale and Synergies: As a platform company, WSP acquires smaller engineering firms, enabling diversification, cross-selling opportunities, and immediate earnings accretion while transitioning private valuations to public multiples.

- Exposure to Global Infrastructure Buildout: Benefits from long-term demand for engineering consulting in infrastructure projects worldwide, including recent US power grid expansion, positioning it for sustained growth despite short-term government spending fluctuations.

- Undervalued with Earnings Upside: Trades at a discounted forward multiple (e.g., 12x two-year-out earnings vs. historical 14x), with potential for faster-than-expected growth and multiple expansion, outperforming industrial peers.

GE HealthCare (GEHC)

- AI Integration for Higher-Margin Products: Pairs AI software with hardware like CT scans and MRIs, acquired through deals like Mim Software (noted as Intelad in discussion), reducing reliance on high-cost radiologists and enabling SaaS models for lucrative upgrades.

- Global Market Leadership and Risk Resolution: Competes effectively against peers like Siemens and Philips in medical imaging, with tariff and China market concerns addressed via third-party arrangements, securing ongoing sales in a competitive landscape.

- Significant Undervaluation and Price Upside: Currently trading around $80 but estimated worth in the $90s, offering a strong healthcare option with low valuation despite recent underperformance, driven by AI-driven innovation.

Brookfield Infrastructure (BIP)

- Exposure to Data Center and AI Buildout: Provides essential utilities and infrastructure for data centers, positioning it as a “secret AI stock” with growth across all divisions tied to high-demand sectors.

- Attractive Yield with Robust Growth: Offers a ~5% dividend yield combined with up to 9% annual growth in funds from operations (FFO) per share, delivering a growthier alternative to traditional utilities with low risk.

- Clean Accounting and Transparent Assets: Features straightforward, predictable assets with clean financials compared to other Brookfield entities, supported by strong management and access to low-cost institutional capital for reinvestment.

Don’t miss our next episode!

![]()

DISCLAIMERS: This text AI generated and should be checked against actual delivery. The content provided in this podcast is for informational purposes only and does not constitute financial, investment, or professional advice. The views expressed by the host and guests are their own and do not necessarily reflect the opinions of any organization or company. The host and guests may maintain positions in any securities discussed on the podcast. Always consult with a qualified financial advisor or professional before making any investment decisions.