AI has driven tech stocks to new heights — but are we starting to see cracks in the story? Shane Obata of Middlefield tells us whether the AI trade is running out of steam or just gearing up for its next phase. From Nvidia’s dominance to rising capital costs across the sector, Shane explains where investors should stay cautious and where the next wave of profits could come from — and why, in this market, all roads still lead to OpenAI. Listen on Apple, Spotify, or YouTube.

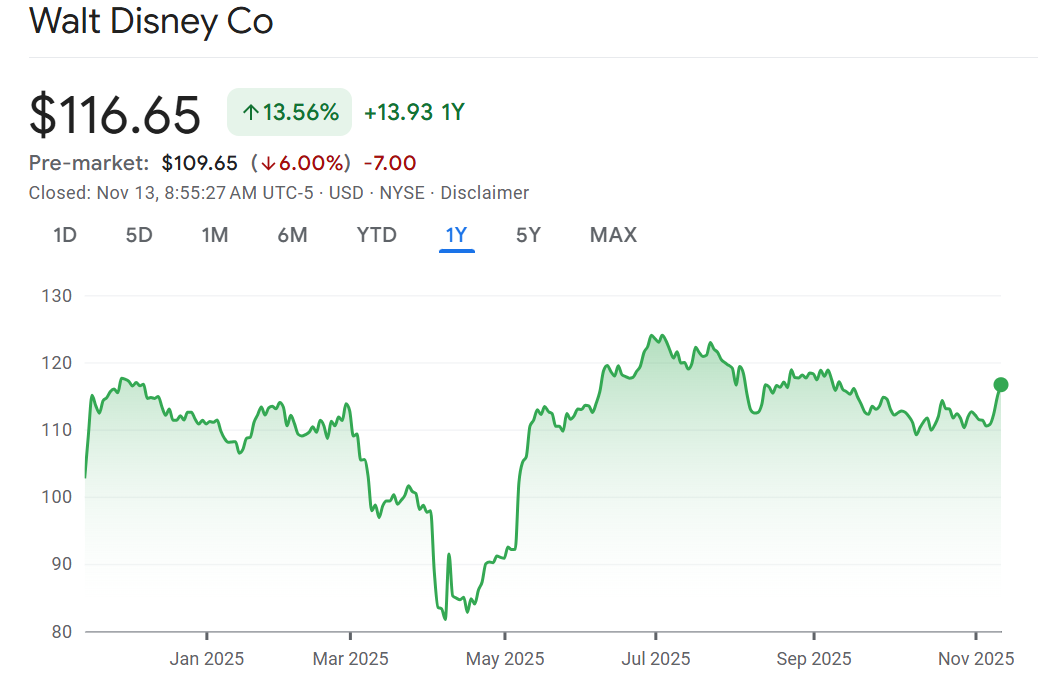

After looking at my bank statements, I am expecting a personal shoutout in Disney’s financial results this morning.

Here are five things to know:

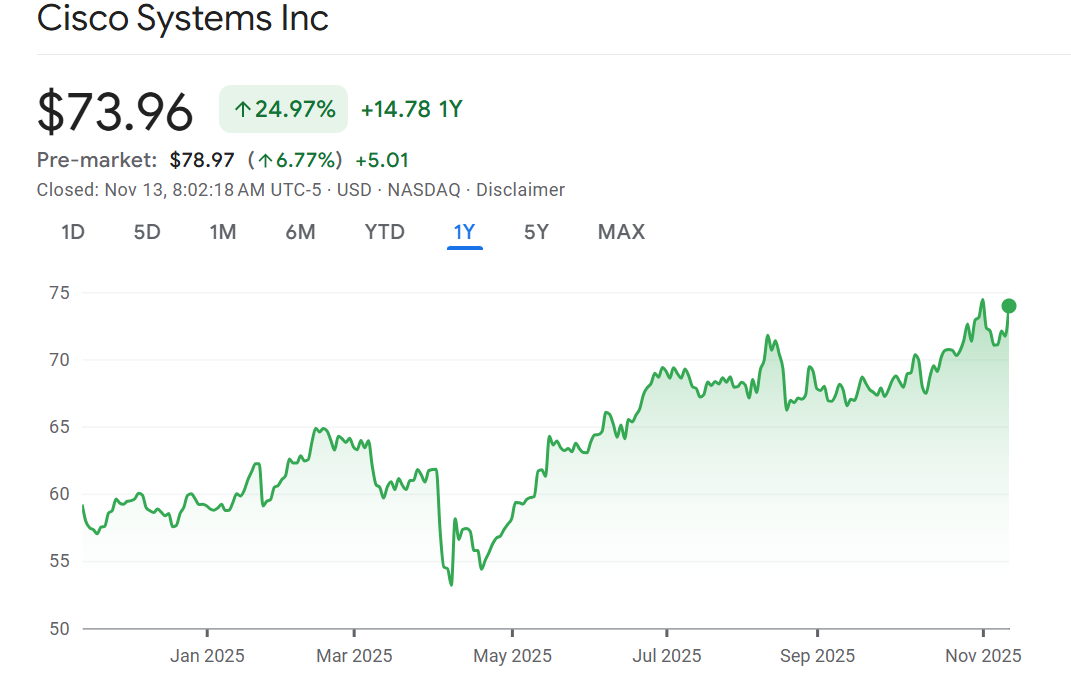

Take on me: While US markets struggled yesterday, the TSX surged to a record high thanks to a rally in gold stocks. Tech stocks underperformed, but the Dow Jones Industrial Average also finished at a record high thanks to financials and health care. This morning futures are indicating a softer open as enthusiasm for the government reopening gives way to anxieties about what the pending flood of economic data will show. Central bankers in the US are out on the circuit discussing the rate outlook with two Fed Presidents (Boston’s Collins and Atlanta’s Bostic) saying rates should stay on hold until inflation cools. The AI trade is alive and well with Cisco ripping higher (more below). But the bull market rally has claimed another victim: Michael Burry of the Big Short fame is shutting down his hedge fund. After making headlines just a week ago about shorting Nvidia and Palantir, Burry’s fund has been deregistered according to SEC filings. Burry has been vocal about accounting chicanery at the big tech companies in which they are “under” depreciating their investments, allowing them to show higher earnings. What’s that saying? The market can stay crazy longer than you can stay solvent. Today there are 15 companies reporting on the TSX including Atkins Realis this morning, and South Bow and Stantec after the bell.

Party like its 1999: Cisco is popping 7% in the pre-market after beating expectations and boosting its sales and profit forecast for the year. The world’s largest maker of networking gear grew sales at 7.5% this quarter but said AI sales will triple from last year to $3 billion (out of $60 billion in total sales). “Fundamentally, Cisco is benefiting from networking upgrade cycle…driven by high agentic AI inference demand,” wrote Citi’s Atif Malik. Shares of Cisco are up 30% so far this year and are $2/share away from the all-time high reached in 2000s. Today could be the day, the number to beat is $80.06/share.

House of mouse: Disney is under pressure after fourth quarter sales missed expectations. On the plus side it added more Disney+ subscribers than expected and boosted its free cash flow outlook. However, their spending plans came in higher than anticipated. It faces a number of headwinds in its entertainment business. First, without an election cycle there are fewer political ads. Second, the cost of marketing its movie slate including Zootopia 2 and Avatar will take a bite out of earnings. Third, streaming profit is growing but not as much as Wall Street hoped. The parks was a bright spot, growing 13% from last year. That unit has been a huge driver of profit this year. But even with all these issues Disney increased its dividend and doubled its share repurchase plans.

Getting realis: Atkins Realis reported better than expected sales and profit this morning. The engineering and construction firm lowered its forecast for sales growth in the engineering unit but increased it for the nuclear unit. Thanks to a boom in nuclear energy demand, ATRL’s division saw sales jump 62% this quarter – almost all of it organic growth. It’s backlog reached a record high. However, this is being offset by weakness in engineering because of a softer outlook in places like the US & Latin America as well as the Middle East. The former SNC Lavalin has been a beneficiary of government spending on infrastructure and more recently a resurgence of nuclear demand. However, the stock has come off recently on conerns about softness in the engineering unit. “With (speculative) nuclear names cooling off … the theme is still very much alive and attracting investor attention,” wrote National Bank’s Maxim Sytchev, “But we need to remind investors that close to 80% of value in the company’s (net asset value) is Engineering-related and here the growth curve has markedly slowed.”

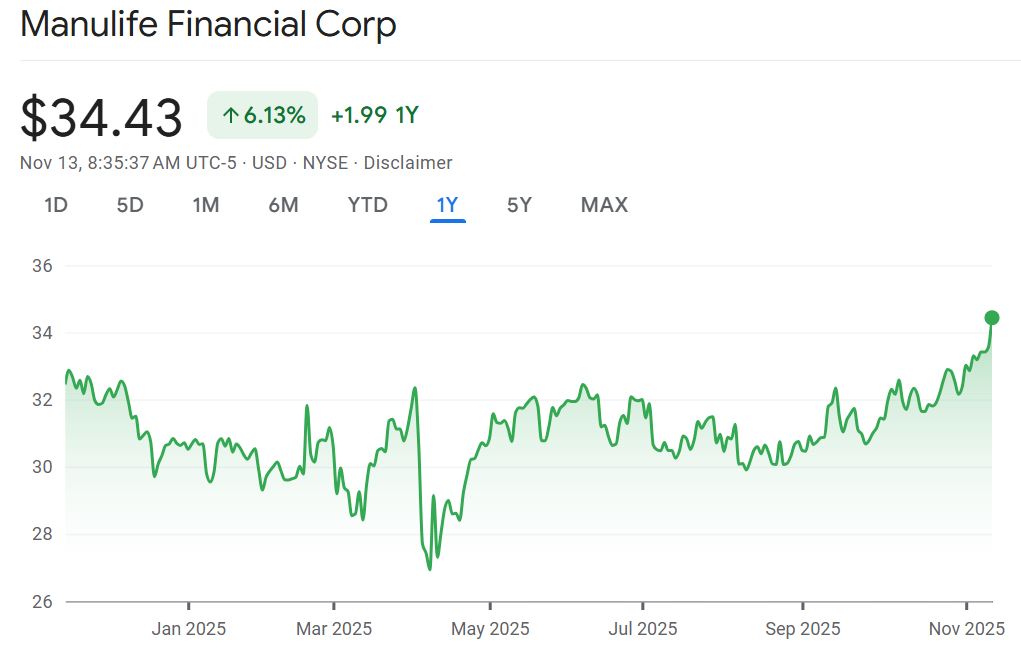

Signs of life: Watch Manulife at the open after profit beat expectations but details were a little fuzzier under the surface. On the plus side: core earnings were better than expected, core return on equity of 18% is right at their target, core earnings in Asia surged 28% while Canada was also strong. Negatives include the fact that part of the profit beat was due to lower taxes and returns in the market were lower than expected because strength in equities was offset by assets in their alternative and long duration business (real estate, infrastructure etc). Bottom line from Gabriel Dechaine at National Bank: “Though MFC’s Q3/25 beat was driven by some unsustainable items (e.g., low tax rate, credit provision reversals), we view the quarter overall as a positive one.”

Get your questions in NOW! Email questions@inthemoneypod.com

![]()