Wall Street meets real talk in this week’s In the Money with Amber Kanwar, featuring none other than Downtown Josh Brown — the CEO of Ritholtz Wealth Management, CNBC regular, and host of the hit podcast The Compound and Friends. From surviving the chaos of the 2008 financial crisis to building a wealth management firm with billions under management, Josh shares how storytelling, not spreadsheets, shaped his investing journey.

Apologies for the absence yesterday, I was hosting the CI Leadership Forum and ran out of morning hours. In full transparency, while I wasn’t paid for the event, I did walk away with one Labubu. Emerging markets manager Matthew Straus had brought it as a prop for his talk on Pop Mart (the maker of those eerie little creatures). My first question to him, in front of 300 advisors, was: “Can I have this Labubu?” Not my most professional moment, but all I could think about were my poor, Labubu-less children at home – social outcasts in a world of furry, unsettling toys.

Here are five things to know:

Peace: North American markets fell yesterday as gold slipped from a record. With the help of the US, Israel and Palestine agreed to a peace framework that would see the release of hostages taken two years ago. Great news for humanity, but the market tends to care not for such things. Gold had its worst selloff since August down 2.4%, oil slipped below $62 barrel. With the US government still shutdown, Fed Governor Christopher Waller gave an interview saying there are alternative data that can be used. Waller, who is in the running to replace current Fed Chair Jerome Powell, signaled he would like another rate cut and that the employment picture in the US is “negative’ and “weak.” Futures are up slightly following those comments. On the periphery, markets are watching a potential collapse of Japan’s ruling coalitian that would have installed the country’s first female Prime Minister. Recall, Sanae Takaichi became leader of the ruling party in a surprise outcome. Her platform called for fiscal stimulus that had many comparing her to Shinzo Abe (aka Abenomics). Then the ruling party’s junior coalition partner quit. It is all very much in flux and the yen got tossed around but doesn’t seem to be a factor in North American markets right now.

Stunner: Canada added way more jobs than expected in September, exceeding even the most optimistic estimate. Canada added 60,400 new jobs vs the expected gain of 5,000. The unemployment rate held steady at 7.1%. Full time jobs led the way with 106,000 new positions. Part-time employment fell 45,600. There were big gains in public sector employment (+30,000), but there were also gains in private sector (+22,000). The Canadian dollar spiked 0.25%, bouncing from a five month low. The odds of a rate cut this month came down dramatically, from 57% chance yesterday to just 36% chance today. “However, the headline gain needs to be viewed in the context of what preceded it,” wrote CIBC’s Andrew Grantham, “…That weakness in July/August means that even after today’s data the 3 and 6-month averages remained soft at -15K and +9K respectively.” Grantham believes that a rate cut will still happen but perhaps this shifts the timing. “Overall, today’s data still suggests that a large degree of slack remains within the labour market, which we think justifies a further interest rate cut from the Bank of Canada, although today’s strength in employment could delay the timing of that move, particularly if the upcoming CPI print is also stronger than expected.”

Anotha one: Shares of Applied Digital are soaring nearly 30% in the pre-market on what is becoming a familiar song in the market. The data centre and infrastructure company announced it is finalizing a lease agreement with CoreWeave for additional data centre capacity first campus. It also said it is near a lease agreement with an investment grade hyperscaler for its second data centre campus in North Dakota. The announcement was part of quarterly results that came in well above expectations.

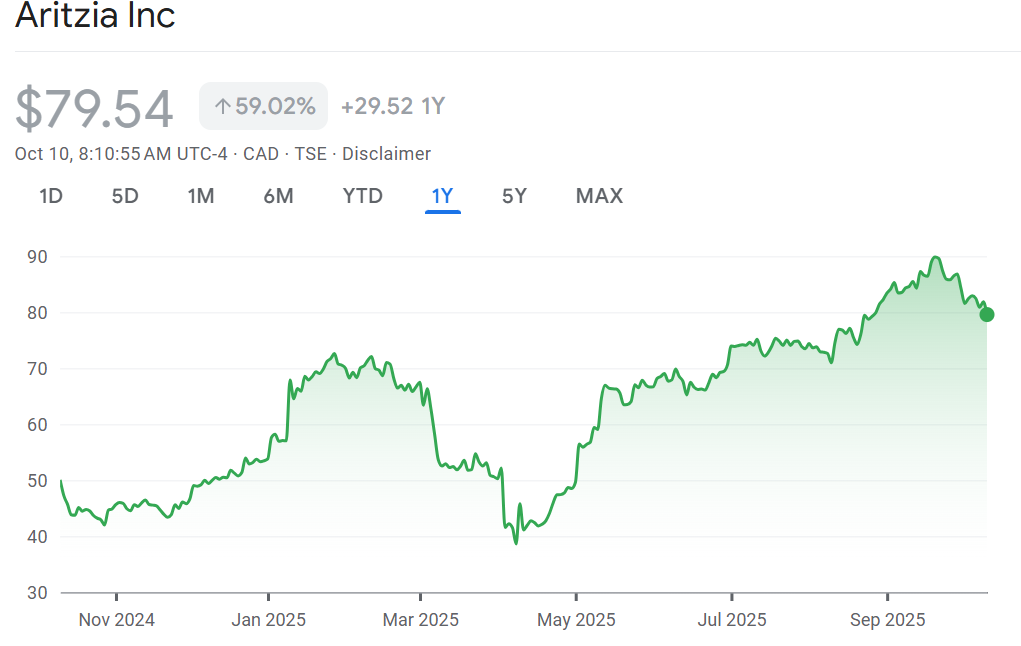

Retail therapy: Watch Aritzia at the open after profit soared past even the highest estimates and sales were double the estimate. Comparable same-store sales grew a whopping 21.6%, the second best performance in three years and far better than the 11.3% growth expected. Margins actually increased despite higher tariffs and the removal of the de minimis exemption in the US. The company’s forecast for sales also came in above expectations. In other words, it was a perfect quarter. But of course the stock is expensive. “Our target multiple is at a premium to the historical average for the stock since IPO and remains at a premium to peers,” wrote Michael Glen of Raymond James, “We believe that this premium is warranted given the opportunity that still exists in terms of new store openings, square footage growth, and digital / commerce initiatives.” Even though their forecasted results are better than expected, Glen believes it could be conservative because it doesn’t include the rollout of their international website and mobile app launch.

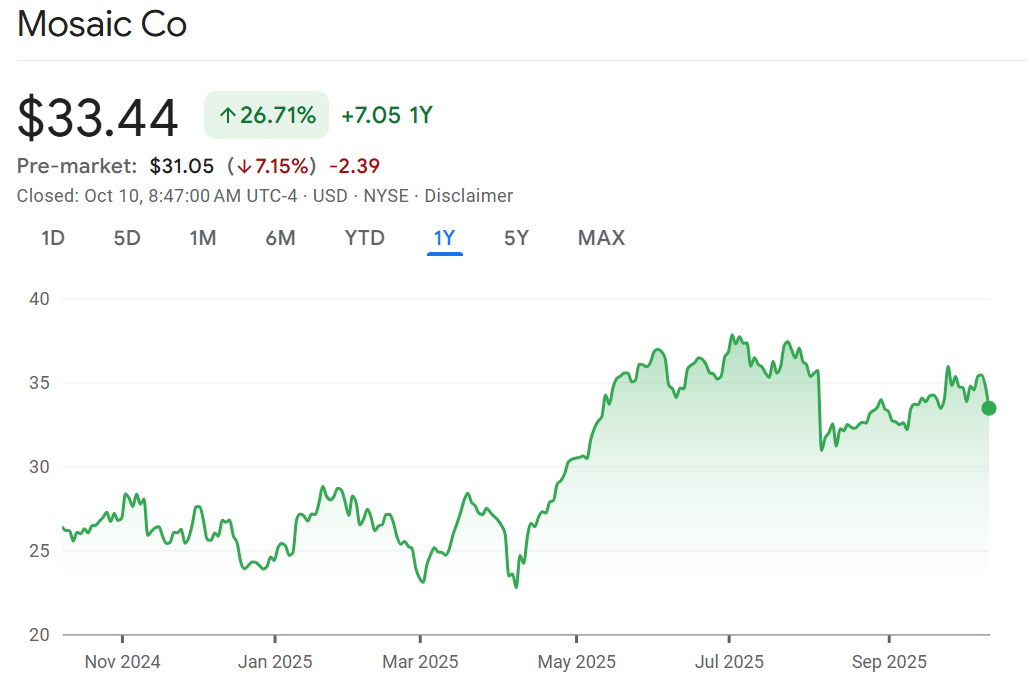

Fertilizer show: Mosaic is falling 9% in the pre-market after warning third quarter phosphate production will fall below expectations because of plant interruptions. The fertilizer giant said they faced “unexpected mechanical issues” in September that caused a “meaningful decline” in overall production. This is not the first time Mosaic has had production issues said Ben Isaacson of Scotia in a blistering note downgrading Mosaic. “We expect the stock to underperform near-term, as credibility questions will resurface, again,” wrote Isaacson. In the second quarter, Mosaic promised that the third quarter would be better. Now they are pushing it out to the fourth quarter. “Perhaps, (Mosaic) should just consider showing the market results, instead of promising,” concluded Isaacson.

don’t miss our next show!

![]()