It’s a monster week with Nvidia reporting quarterly results just as tech stocks are wobbling. Will Nvidia save the day? Read my preview in the Globe and Mail.

Here are five things to know:

Lucky 11: The S&P 500 has been higher every single Monday for the last 10 Mondays…will today be 11? Now that I have written about the trend, the answer is probably no. Indeed, futures are losing ground this morning as investors look toward Nvidia results Wednesday and the release of September jobs data on Thursday morning. The market is reducing the odds of a December rate cut, which is sitting at a 41% chance right now. Tech stocks are strong this morning after Samsung hiked the price of memory chips. Shane Obata of Middlefield touted Samsung on the podcast last week on this very catalyst.

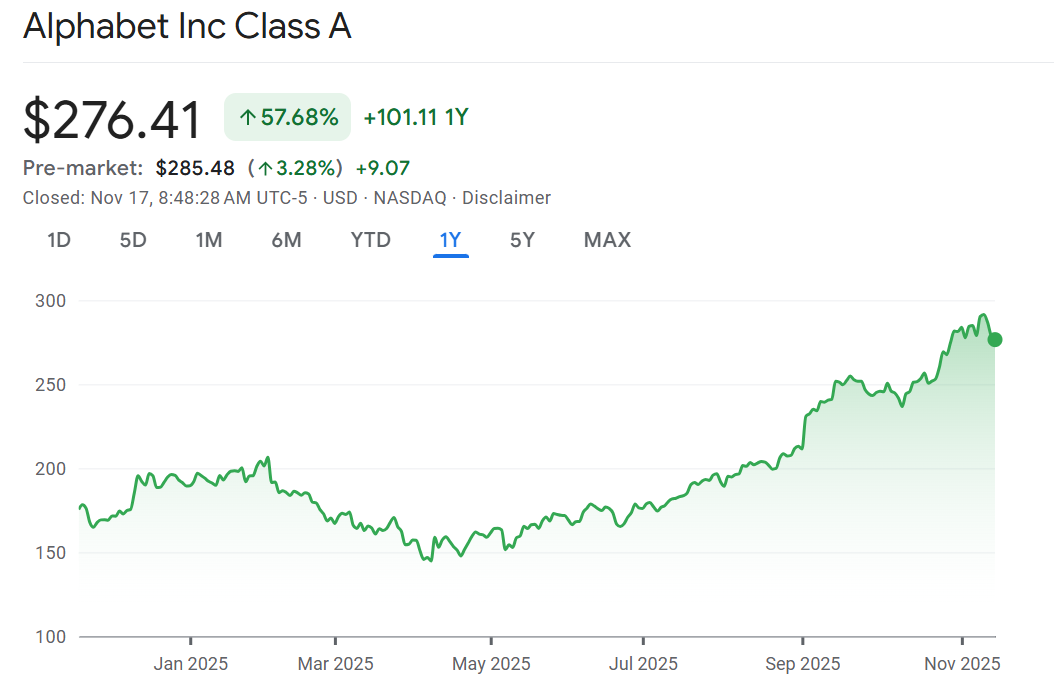

What the 13F: Alphabet is up 4% in the pre-market after Berkshire Hathaway revealed a $5 billion stake in the parent company of Google. 13F filings showed Berkshire added Google while continuing to trim its position in Apple cutting that stake by 15%. Even with the addition of Google to the portfolio, Berkshire was still a net seller of stocks and sits on a record $382 billion in cash. It’s a classic buy for the value investor: Google is the second cheapest Magnificent 7 stock (Meta is now the cheapest after its sell off). I continue to kick myself for selling Google after the Dan Niles episode where I let my ChatGPT fears get the better of me.

Getting colder: Inflation in Canada cooled down in October both on a headline and core basis. Headline inflation rose only 2.2% from last year. While that was higher than expected, it is a slowdown from 2.4% the month before. Core inflation was lower than expected at 2.9% marking the first time since March we’ve seen a reading below 3%. The declines were driven by lower gas prices and slower food inflation. Still, these are uncomfortable levels of inflation for the Bank of Canada and support their decision to pause interest rate cuts. “Overall, while inflation decelerated in October, the move was in line with expectations and it would take a longer period of easing price pressures, combined with indications of economic growth deteriorating again, to bring the Bank of Canada back off the sidelines,” wrote CIBC’s Andrew Grantham.

Rumour has it: Watch Barrick Mining after Reuters reported the company is considering splitting its North American business from its African & Asian mines. If they do that, they would essentially undo the merger with Randgold in 2019 and shed assets brought in by former CEO Mark Bristow. Maybe that explains why he left suddenly at the end of September. (The Globe’s Niall McGee has great reporting on the personality clash between Bristow and Chair John Thornton). All of a sudden, Rob Lauzon’s prognostication on the podcast that Barrick and Newmont will do a deal (they have a JV together in Nevada) starts to look like more of a possibility. While this is all rumours, clearly something is afoot with Bristow’s departure. “With (Barrick) undergoing a management transition, it is possible they are exploring options to surface value,” wrote TD’s Steven Green on the Reuters report, “Based on our sum of the parts valuation, this could work, pointing to 29% upside.” While Barrick has had a tremendous rally in the past year, it is still trading at a discounted valuation argues Green. “…We highlight (Barrick’s) valuation discount to peers, which we view as unwarranted given the upside potential value in the 100%-owned Fourmile discovery, and the value of a large long-life asset in a Tier 1 jurisdiction like (Nevada) (which they operate and own 61.5%). NEM, in particular, which trades at a premium to B, would be a likely acquirer of these assets.”

Notable calls: National Bank is downgrading BMO and upgrading Royal Bank. Shares of BMO have rallied as credit quality improved from dismal levels last year. National Bank’s Gabriel Dechaine says that catalyst has worn itself out and now that US loan growth is stalling he doesn’t see much upside from here. On the flip side, Dechaine is upgrading Royal Bank. “…We believe it offers an attractive combination of upside elements (e.g., Capital Markets momentum, ROE upside potential) and its potential for outperformance in a more negative market scenario,” he wrote in the upgrade. Shares of Dell and HP are falling in the pre-market after Morgan Stanley’s Erik Woodring downgraded the stocks on a “memory” super cycle that would increase costs for original equipment makers. Refer to the Obata link above for what is going on in memory, but basically prices are going up on a big supply crunch. Great if you are Micron or Samsung, not so great if you have to buy those chips (Dell and HP).

Don’t miss our next episode!

![]()